Without knowing your break-even point, you can’t make informed business decisions.

To cover the costs of your business you need to sell enough goods or services to reach your break-even point. Knowing where that point is, and how long it will take you to reach it, can be fundamental to your success. This especially true if you’re thinking about starting or buying a business.

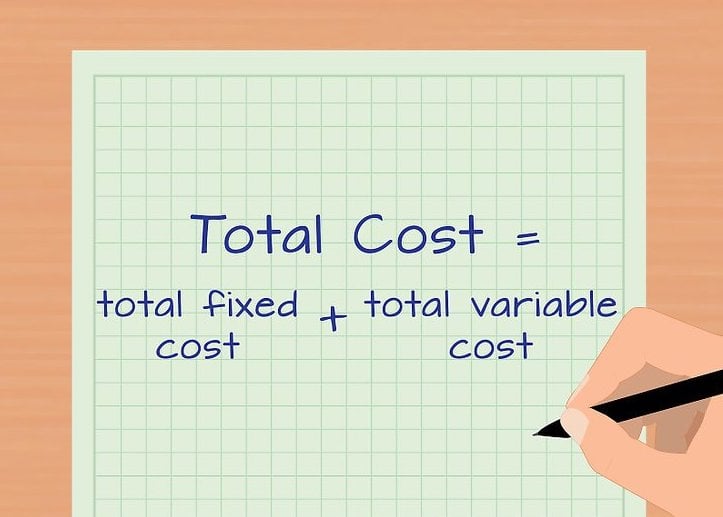

Calculate fixed and variable costs

The first step is to establish your fixed and variable costs.

Fixed Costs

Fixed costs are bills your business always has to pay, regardless of its level of sales. Also known as overheads, they could include:

-

Salaries for permanent staff.

-

Rent on your premises.

-

Insurance.

-

Interest on debt.

Variable Costs

These are costs that increase with your levels of sales – materials and production costs are two examples. Others include sales bonuses, part-time wages and freight.

Now work out:

-

The total fixed costs bill for the year.

-

An average overall variable cost for each product or service sold (the Variable Cost per Unit).

Some bills might be a combination of fixed and variable costs, such as a phone bill split between a line cost and toll call charges. Separate these bills into fixed and variable parts for greater accuracy.

If breaking them up is too time consuming, choose which element is greater in the bills and classify it as that. For example, if you don’t make many calls to mobile phones or outside your local area, you’d classify the phone bill as being fixed.

Determine your break-even point

Let’s assume you manufacture shoes with the following details:

-

Budgeted fixed costs of $60,000.

-

Average cost to make a pair of shoes is $110.

-

Average sale price per pair of shoes is $250.

Calculating your break-even point requires the use of a few formulas:

-

Sales Price per Unit ($250) minus Variable Costs per Unit ($110) = Contribution Margin per Unit ($140).

-

Contribution Margin per Unit ($140) divided by Sales Price per Unit ($250) = Contribution Margin Ratio (0.56).

-

Fixed Costs ($60,000) divided by Contribution Margin Ratio (0.56) = Break-even Sales Volume ($107,142).

Based on these calculations, if you sell more than $107,142 of shoes you’ll make a profit. That equates to 429 pairs.

Using your break-even point

Once you’ve worked out your break-even point, the next step is to work out whether the sales volume you’ll need to break even is realistic and achievable.

You can also use your break-even calculation to see the effect of changes in costs on your business. If you were able to source cheaper materials and reduce the variable cost per pair of shoes, you’d need to sell fewer pairs to break even.

If your sales remained the same, you’d make more profit.

To be of real value to you, your fixed and variable costs calculations need to be accurate. Putting inaccurate figures into your break-even calculations will give you an inaccurate result. It’s worth investing time to work out your figures accurately.